- Navigator

- Expansion Solutions

- Finance & Insurance

- Industry Analytics

Editor’s Note: This article was originally published in the May/June 2021 edition of Expansion Solutions.

There is not a local, regional, or state economy that does not include multiple businesses and considerable employment in finance and insurance. From the small bank branch, credit union, or insurance agency office to the larger regional hubs and corporate headquarters, all areas of the country have finance and insurance in their economic mix. Like all industry sectors finance and insurance is changing rapidly through new technology, changes in the workforce, and evolving consumer and business preferences. In the article we provide an economic overview of the finance and insurance industry including recent and projected trends, areas of industry growth and concentration in the U.S., and factors driving this growth. This information will help economic developers with their strategies for leveraging these important industries.

Finance and insurance is a broad industry category that includes establishments primarily engaged in financial transactions (transactions involving the creation, liquidation, or change in ownership of financial assets) and/or in facilitating financial transactions[1]. Three principal types of industry activities are:

The key subsectors within Finance and Insurance are:

We examine these sectors along with the specialized connection to emerging tech, specifically fintech and insurtech.

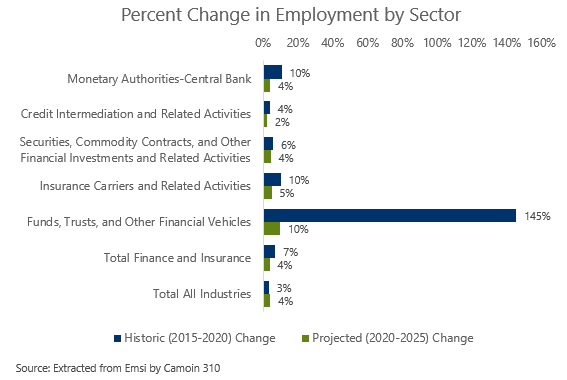

Finance and insurance industries represent 4% of all employment in the US and their growth has been outpacing the economy as a whole.

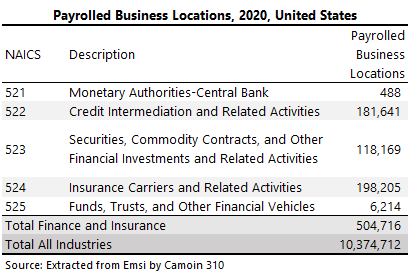

There are an estimated 504,716 business establishment finance and real estate representing 5% of all business establishments in the U.S. The largest sub sectors of finance and insurance are commercial banks and credit issuers, insurance carriers, and brokerages, which together represent 75% of all establishments in the industry.

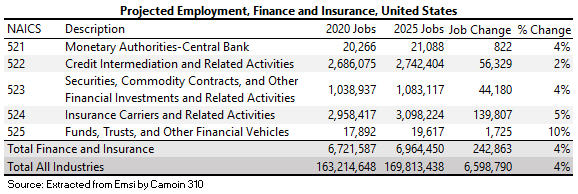

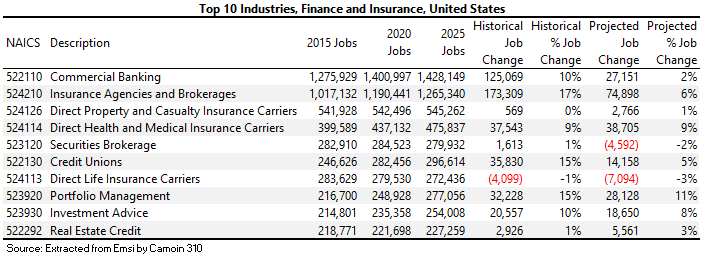

Looking deeper into industry subsectors two 6-digit subsectors dominate the industry: commercial banking and insurance agencies and brokerages. Together in 2020 they accounted for 39% of all jobs in finance and insurance in 2020. Insurance agencies and brokerages are projected to continue robust growth of 10% through 2025.

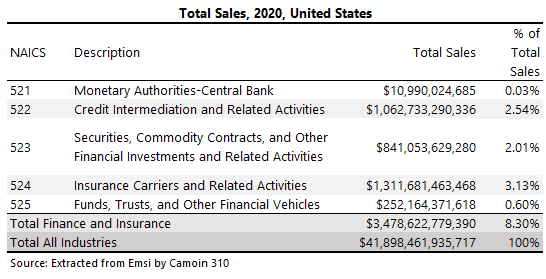

Total sales in finance and insurance were nearly $3.5 trillion in 2020 representing 8.3% of all sales in all industries in the U.S. This is a higher percentage than employment, attesting to the high economic value of the industry.

In the five years leading up to COVID improvements in the economy led to the release of pent-up industry demand. As we recover from COVID demand will increase once again, creating opportunities for industry and employment growth.

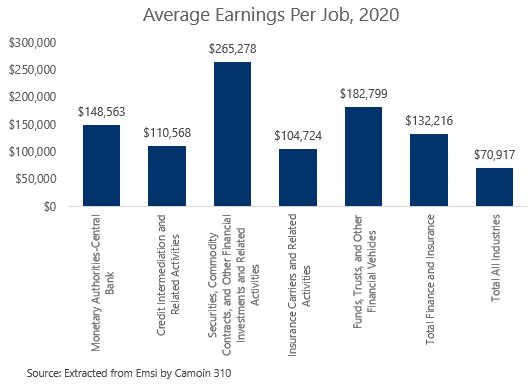

Average annual earnings in Finance and Insurance were $132,216 in 2020, considerably higher than the $70,917 for all industries, again attesting to the high value of these industries.

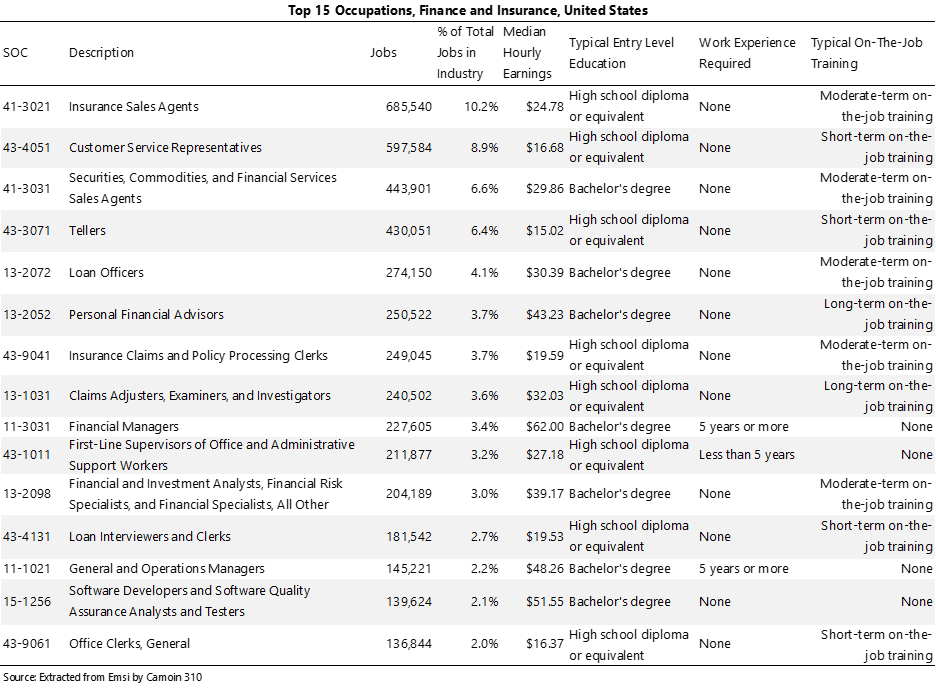

Finance and Insurance incorporates a variety of occupations with most being in sales, customer service, management, and analysts. Whiles many require four-year degrees, there are many that do not including sales customer services and clerks. Additionally, there are plenty of entry and mid-level jobs with career paths for advancement. Insurance however does require advanced mathematics for jobs such as actuarial, and demand for computer and software skills are increasing across all of finance and insurance.

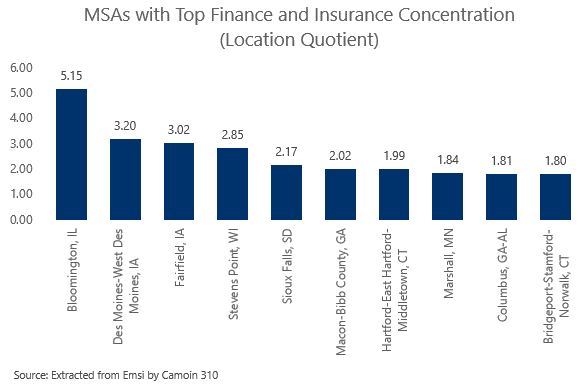

Overall finance and insurance industries exist in every region and state as they include both local services and branches as well as regional hubs and national headquarters. Some metro areas however are highly concentrated in terms of employment in these sectors including Bloomington IL, home to State Farm Insurance; Des Moines IA, home to Wells Fargo; Stevens Point WI home to Sentry Insurance; Sioux Falls SD home to multiple insurance, bank, and credit card companies; and Hartford CT home to multiple insurance companies. These are in addition to some of the larger metros in terms of number of employees including New York City NY, Dallas TX, Charlotte NC, Phoenix AZ, Salt Lake City UT, Miami FL, and Detroit MI.

Digging deeper into the key subsectors of commercial banking and insurance agencies and brokerages and looking at establishments the Southeast, and specifically Florida, has among the highest concentrations of commercial banking establishments. The Southeast has the largest proportion of establishments, estimated at 28.0% in 2020. This region includes some major economic states, such as Florida (6.0% of establishments), North Carolina (3.2% of establishments) and Georgia (3.0% of establishments)[2].

The largest players across the nation include:

Together these companies account for approximately 27% of industry market share.

California, Texas and Florida have the highest share of insurance agency and brokerage establishments. The Southeast region is also highly concentrated, accounting for 25.2% of total industry establishments. Within the Southeast, Florida contains the third-highest share of establishments in the country, with 6.9% of the total in 2020[3].

The largest players across the nation include:

So, what drives location decision in finance and insurance?

As mentioned above the local market, driven by number and concentration of people and businesses, does matter. Specifically, it matters for those segments of the finance and insurance industry that rely on customer facing interactions and relationships such as local branches, sales entities, and customer service. This includes the small to mid-size insurance agencies, financial advisories, and local and regional bank branches.

For larger businesses including back offices and national and regional headquarters, according to Wes Edwards, business engagement and attraction expert at Camion 310, there are two key factors that influence location decisions:

In addition to these it is a given that digital infrastructure and quality places conducive to talent attraction and retention are a given for success.

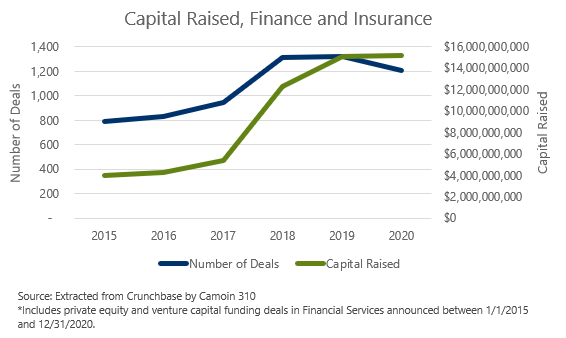

Finance and insurance industries are raising and increasing amount of capital financing.

Since 2015 the amount of capital raised in finance and insurance increased from $4 billion to more than $15 billion annually. 1,207 deals were announced in 2020.

Like nearly all industries and industry subsectors, finance and insurance is experiencing dramatic changes and in some cases significant disruptions. These have many causes of these changes, including evolving consumer preferences, new technology, the financial collapse of 2008, new regulations, COVID-19, changing workforce patterns, and more. Below we highlight some of the major factors and the challenges and emerging opportunities they present.

Technology is continuing to change rapidly creating disruptions and opportunities.

This includes:

Value of data and information to industry balanced against privacy and security – cybersecurity, personal control of data – trust as currency to make opportunities real.

Social Equity – cultural changes for products and services that address and adhere to social good – this includes both the need to get banking and investment services to more people and specifically more diverse populations of minority communities, minority and micro businesses, startups, and neighborhoods as well as investing with social purpose and investing to support social challenges such as poverty, climate change, inequality. This emphasis on social good has resulted in the increase in Environment, Social and Governance (ESG) investing.

Changing workforce including the need for digital skills, advanced IT integration, and remote work – work from anywhere and hybrid work at place and home are here to stay in some capacity. This further creates increased need for broadband and cybersecurity. It also significantly impacts real estate space demand which in turn impact community economic impacts. In addition, the workforce skills needed to support the industry are becoming increasingly advanced digital and analytic, mixed with customer service.

Continued and ever-changing regulation to address security, social equity, and competition create both constraints and opportunities – regulation has always been part of the modern finance and insurance industries. However, the new and rapidly changing challenges presented by technology, consumer protection, security, privacy, and competition is creating new regulation with more on the way as political governance “catches up” with some of the trends. In turn, finance and insurance regulation is also creating opportunities for new services and businesses.

Need for new business models – all these factors require new business models for success. PwC documents the impact of disruption and therefore the need for new business models. “In our recent PwC Global FinTech Survey, industry respondents told us that a quarter of their business, or more, could be at risk of being lost to standalone FinTech companies within five years.” [5]

One need not look any further than the behemoth that is Amazon for major potential disruption. According to CB Insights: “it’s hard to claim that Amazon is building the next-generation bank. But it’s clear that the company remains very focused on building financial services products that support its core strategic goal: increasing participation in the Amazon ecosystem.[6] And a large ecosystem it is! New entrants, large and small will continue to present both challenges and opportunities within finance and insurance.

So, what does this mean if you are an economic developer seeking to support and harness opportunities and better prepare for challenges for economic growth in your region? The following provides some strategies and examples for getting started.

This includes working with public and private partners to provide access to and greater understanding of personal and commercial lending including micro loans. Local bank branches along with smaller local financial entities including credit unions and community development financial institutions (CDFI’s) are partners to be leveraged. CDFI’s are “community development loan funds, banks, venture capital funds, and credit unions that provide fair, transparent financing and financial education to small businesses, community-based projects, and consumers that mainstream finance considers too risky or not profitable enough.” [7] These efforts have the dual impact of increasing the market for business and financial services and increasing economic development and opportunity overall by accessing underserved markets. The State of Rhode Island is currently embarking on a statewide effort to increase access for minority populations and businesses through a partnership with RI Commerce, Rhode Island Foundation, and the Multicultural Innovation Center.

Finance and Insurance are diverse industries. It is difficult for economic regions to be specialized in each diverse subsector and cross sector opportunity such as fintech and insurtech, finance, insurance, investment banking etc.… Success requires supporting a business environment conducive to all businesses and workforce but then knowing where you need to spend extra attention for deeper strategies and tactics to meet unique needs. The state of Florida does this well. With one of the largest amounts of finance and insurance activities, the state leverages its overall positive business environment with a focus and alignment on regional industry niches including investment banking in the Jacksonville region; fintech and international banking in Miami and South Florida or “Wall Street South”; back office, mid office, and regional headquarters for treasury, accounting, and finance in Tampa Bay and Orlando to name a few. This is achieved by strong support and focus from the Governor’s office, to Enterprise Florida, the state economic development organization, down to the regional and local economic development entities.

This can be done through partnerships and alliances with industry associations and chambers of commerce.

Like all industries finance and insurance are increasingly complex cutting across sectors, occupations, and issues. Success requires a dense ecosystem of connections among, information technology, analytics, and cybersecurity as well as R&D, accelerators, incubators, support services, workforce entities, and the businesses themselves both large and small.

Help starts up and small companies get connected to larger customers/legacy companies. Columbus, Ohio is home to major legacy companies finance and insurance and insurance including Nationwide Insurance and JP Morgan Chase. To leverage this history with emerging fintech Fintech71, an accelerator that provides intensive services within cohort classes and connects with mentors from legacy companies, was established in 2017. It is also supported by strong partnerships for services through providers such as Rev1 Ventures which has a strong history of helping companies start and scale and obtain capital.

As mentioned previously, workforce is one of the top if not the top issue for growing your region in finance and insurance. And while there are multiple types of jobs and skills needed that run the gamut similar to other professional business, some of the skills are both particularly critical and hard to come by, including actuaries. Realizing this ongoing need for the success of its industry, the Hartford Connecticut Region, touted as the Insurance Capital of the US, developed the Actuarial Boot Camp. This is an “immersive, interactive experience taking students inside the actuarial profession for a springboard to future success! It provides high school and college students the opportunity to find out if an actuarial career is for them and features in-depth math instruction and highlights effective negotiation skills, assessment and risk, case studies and ethics.” [8] The Boot Camp was developed by the Connecticut Insurance and Financial Services industry program of the Metro Hartford Alliance.

Like roads and ports of the past, these are the critical infrastructure needs of today and tomorrow. They are needed by all industries but particularly fintech and insurtech.

This includes working with local banks, credit unions, financial advisors, and insurance agencies to create great place-based environments for networking and business development opportunities. Chelsea Groton Bank in Groton Connecticut understands this importance and has begun to remodel its branches to be both places of business and places for networking within the community. When the Town of Groton launched it Town and City Joint Economic Development Plan, Chelsea Groton Bank gladly hosted free and open discussions on the plan among the public and business community. This provided an atmosphere that was conducive to open engagement and connecting.

In an ever changing world economic development requires constant learning and adapting. PWC provides the following advice for finance and insurance industries in light of emerging change and distribution: “you have a choice: to lead the charge, to make sure your organization has the right listening capabilities and agile architecture to be a ‘fast follower’, or to watch others take advantage of a generational shift”. [6] The same is true for economic development overall.

[1] NAICS.com

[2] IBISWorld

[3] Ibid

[4] WNS https://www.wns.com/insights/articles/articledetail/547/top-trends-in-ba…

[5] PwC Global FinTech Survey 2016 as referenced in PwC Financial Services Technology 2020 and Beyond,

[6] Everything You Need To Know About What Amazon Is Doing In Financial Services, 2021, CB Insights https://www.cbinsights.com/research/report/amazon-across-financial-servi…

[7] https://ofn.org/

[8] https://www.connecticutifs.com/ifs-workforce/actuarial-boot-camp/

[9] PwC Financial Services Technology 2020 and Beyond, Page 6, https://www.pwc.com/gx/en/financial-services/assets/pdf/technology2020-a…

[10] Image Source: Adobe Spark and Camoin 310

Workforce Development

What’s the best way to engage with young people in order to pique their interest in career opportunities in different sectors? Find out what a group of high school students recently told our author.

Industry Analytics

Economic & Fiscal Impact Analysis

Your resource for understanding today and looking toward tomorrow

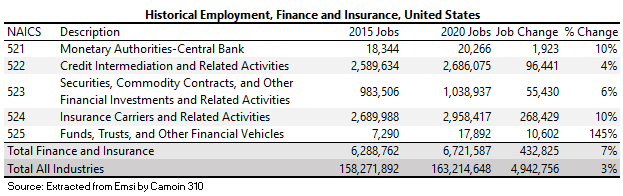

In terms of employment, finance and insurance accounted for over 6.7 million jobs in the U.S. in 2020, representing around 4% of the nation’s jobs. Like with establishments the largest subsectors are commercial banks and credit issuers, insurance carriers, and brokerages. In the past five years jobs in finance and insurance have grown 7%, outpacing overall job growth of 3%. Of the 432,825 jobs added in the past five years, 268,429 or 65% of jobs added were in the insurance carriers and related actives subsector.

In terms of employment, finance and insurance accounted for over 6.7 million jobs in the U.S. in 2020, representing around 4% of the nation’s jobs. Like with establishments the largest subsectors are commercial banks and credit issuers, insurance carriers, and brokerages. In the past five years jobs in finance and insurance have grown 7%, outpacing overall job growth of 3%. Of the 432,825 jobs added in the past five years, 268,429 or 65% of jobs added were in the insurance carriers and related actives subsector.